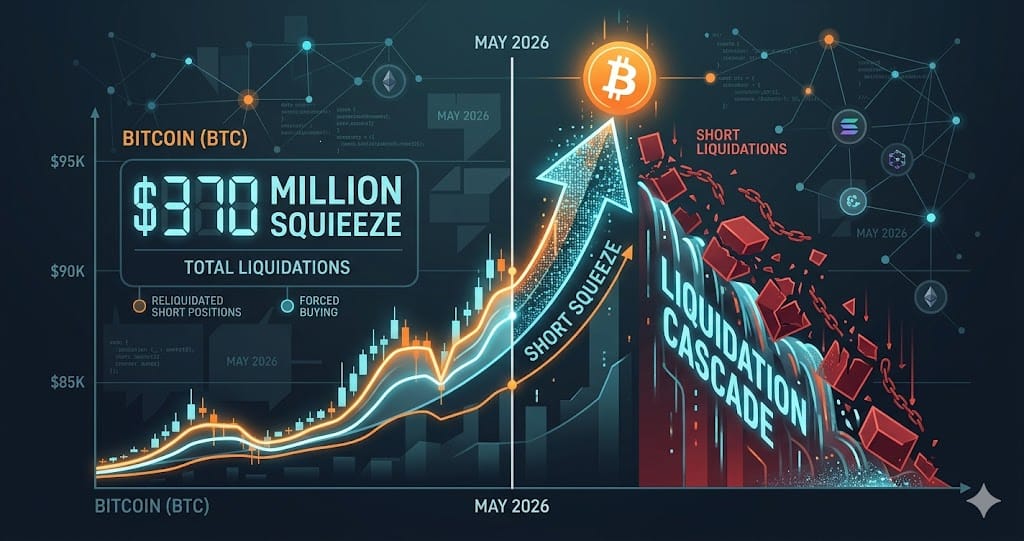

Bitcoin's $370M Short Squeeze: Reading the May 2026 Liquidation Cascade

From $301.93M in BTC shorts liquidated on May 4 to a $415.57M peak on May 7, May 2026 revealed a structural shift in Bitcoin's futures market.

Between May 4 and May 11, 2026, Bitcoin's perpetual futures market cycled through three distinct liquidation waves totaling over $900M cumulative, with 97,235 traders forced out in the May 4 event alone. The data points to a passive mechanism: 67 days of negative funding rate accumulation pressured short positions to a breaking point where price increases triggered forced closures without requiring new long-side buying pressure.

Open interest on BTC exceeded its 2025 all-time high during this window, yet the Crypto Fear and Greed Index held at 49 (Neutral) on May 11 — a reading 10x Research founder Markus Thielen described as 'structural rather than a sentiment shift.' For traders active in leveraged crypto futures, the May 2026 sequence provides one of the clearest documented examples of how funding rate architecture shapes cascade risk across both centralized and decentralized venues.

The Three-Stage Short Squeeze Staircase: April 14 to May 7

The April-to-May short squeeze pattern unfolded across three price thresholds in a near-logarithmic decay of short liquidation size. On April 14, Bitcoin testing $75,000 put approximately $200M in short positions at immediate liquidation risk per CoinDesk data. Four days later on April 18, a break above $77,000 triggered $593M in short liquidations — the single largest event in the sequence. On May 4, Bitcoin clearing $80,000 produced $370M in total 24-hour liquidations with $301.93M from shorts alone, roughly a 4:1 short-to-long ratio, as BTC contributed $179M and ETH contributed $95M of those forced closes.

The May 7 peak of $415.57M covered the $80,000-to-$82,320 push and marked the tail end of the staircase. Reading the sequence in order — $593M in shorts on April 18, then $301.93M in shorts on May 4, then $415.57M total on May 7 — reveals that each event was drawing from a smaller available pool of adequately margined short positions. By May 9, total liquidations had collapsed to $50.26M, an 87.9% drop from the May 7 peak, confirming the short overhang had been substantially cleared. CoinDesk explicitly noted that May 4 was the second occurrence of this pattern within two weeks, treating April 18 as the structural precedent.

Cascade Exhaustion and the Long-Short Flip: May 8 to May 11

The pivot arrived between May 8 and May 9. A second round of U.S. strikes on Iranian oil tankers on May 8 reversed BTC to $79,614, which triggered profit-taking from existing longs rather than fresh short entries. By May 9, Binance's BTC funding rate simultaneously flipped from a multi-week average near -5 basis points to +0.0043% — the first positive reading after the 67-day negative streak — providing a clean real-time confirmation that the structural short imbalance had cleared.

By May 11, total liquidations rebounded to $140.18M, but the composition had inverted for the first time in the cycle: longs accounted for $76M versus $64.18M for shorts, a 1.18:1 long-to-short ratio. This reversal is significant because it signals the end of passive short cascade fuel. CryptoQuant analyst Darkfost issued a parallel warning that the combination of BTC open interest above the 2025 ATH and newly positive funding rates now creates the precondition for a long-side cascade if $75,000 fails as support — a different directional risk than the market faced through April.

Funding Rate Architecture: Why Settlement Frequency Amplifies Risk

The 2026 BTC funding rate averaged 0.51% per 8-hour period across major exchanges, annualizing above 70% — roughly 50 times the neutral baseline of 0.01% per 8 hours. This made funding arbitrage the dominant institutional strategy for the period: holding spot long exposure while shorting perpetuals captured a near-riskless annualized yield above 70%. The 67-day negative funding streak was primarily this phenomenon at scale, not a consensus directional short view. Quantitative desks suppressed the rate structurally while retail interpreted it as bearish signal.

Settlement frequency creates a hidden leverage multiplier that the May cascade exposed. Binance, Bybit, and OKX settle at 8-hour intervals (00:00, 08:00, and 16:00 UTC), while Hyperliquid and dYdX settle every hour. At identical annualized rates, a short on Hyperliquid pays 8 times the weekly funding cost of an equivalent Binance position. This is the microstructure reason the Hyperliquid address 0x128e — holding a $20.3M 40x BTC short with a liquidation price of $82,236 — faced capital erosion disproportionate to the same trade placed on a centralized exchange. Altcoin funding by May 11 showed a synchronized negative-rate cluster: ETH at -0.0038%, Chainlink at -0.0035%, SOL at -0.0036% (before inverting to +0.006%), and XRP at -0.0025%, which Amberdata flagged as a fragile-market signal indicating short crowding had migrated from BTC into altcoins.

James Wynn and the Structural High-Leverage Short Bias on Hyperliquid

The James Wynn case, cross-confirmed by Yahoo Finance and Cointribune, provides the most complete public record of persistent high-leverage short behavior in this cycle. By March 2026 Wynn had accumulated 194 total liquidations. The documented path runs from a $100M account through his largest-ever position — a $1.26B nominal BTC long opened in early 2025 — followed by a $1M loss across May to June 2025, nine liquidations in a single July 2025 week, 45 liquidations across July-August 2025, and an account balance of $900 by March 2026. The 4th episode in April 2026, which was his 6th liquidation within two weeks at that point, falls within the same staircase window studied here.

Wynn functions as a measurable sample of a broader Hyperliquid structural pattern rather than an isolated retail case. Despite the May 9 funding rate flip to positive on Binance, new 40x short entries continued on Hyperliquid: address 0x128e opened its $20.3M position on May 6, the day after the $370M short wipeout. Separately, Hyperliquid BTC long positions simultaneously reached a record high as a different whale cohort accumulated longs, creating what ChainCatcher described as a venue split — on-chain longs versus centralized-exchange shorts — rather than a genuinely mixed market. Binance's aggregate long-short ratio remained at 36.7% long versus 63.3% short through this period, and the structural bearish skew among active futures traders had not materially corrected even after two weeks of short cascade events.

What to Watch

- BTC $75,000 support: a confirmed break below this level is the trigger CryptoQuant analyst Darkfost identified for a long-side cascade, given record-high open interest above the 2025 ATH and recently turned positive funding rates creating a new directional pressure dynamic

- ETH perpetual funding on Binance at -0.0020% paired with open interest at a cycle high of 14.17 million contracts and three consecutive sessions of reverse inflows into Binance — the exact pre-condition setup 10x Research flagged for a potential ETH short squeeze toward $2,600

- SOL long crowding: the 74.2% long ratio with positive funding at +0.006% makes SOL the only major altcoin where a passive short-squeeze mechanism could activate, since short positions there are currently paying premium to stay open against a heavily long-skewed book

- Hyperliquid open interest for new 40x BTC short entries: the May 9 funding flip has not deterred new shorts (0x128e opened May 6 post-wipeout), and the hourly settlement structure means these positions pay 8 times the weekly funding cost of equivalent positions on Binance or Bybit

Ready to start trading?

Trade on Bitget Try CoinTech2uAffiliate links — we may earn a commission at no extra cost to you.

Related Articles

- Bitcoin's 67-Day Funding Rate Flip and Liquidation Storm: May 2026 Analysis

- Crypto Narrative Playbook: May 2026 Market Signals Decoded

- Bitcoin's 67-Day Negative Funding Rate Record and Short Squeeze Setup in May 2026

Frequently Asked Questions

What caused the $301.93M short liquidation on May 4, 2026?

BTC clearing $80,000 on May 4 acted as a forced-close trigger for short positions that had accumulated over a 67-day period of negative funding rates. The mechanism was passive rather than demand-driven: as price rose, shorts with insufficient margin were automatically liquidated by exchanges, which created additional upward price pressure that liquidated the next tranche of shorts in sequence. This cascade produced 97,235 individual liquidations in 24 hours according to CoinDesk, with BTC contributing $179M and ETH $95M of the $301.93M short total. CoinDesk noted it was the second occurrence of this pattern within two weeks, with April 18 at $77,000 having produced $593M in shorts as the structural precedent.

Why did total liquidations drop 87.9% from May 7 to May 9?

By May 7, the pool of short positions carrying insufficient margin at prices above $80,000 had largely been exhausted through the April 18-to-May 7 staircase. The May 8 reversal to $79,614 — triggered by a second round of U.S. strikes on Iranian oil tankers — caused existing longs to take profit rather than new shorts to accumulate. With the short overhang depleted, there was no remaining cascade fuel, and May 9 total liquidations fell to $50.26M. Binance's BTC funding rate simultaneously flipped from its prolonged negative average to +0.0043%, providing a real-time confirmation that the structural short imbalance that had powered the cascade sequence had cleared.

How does Hyperliquid's hourly funding settlement differ from Binance's 8-hour cycle, and why does it matter for liquidation risk?

Binance, Bybit, and OKX settle perpetual funding fees three times per day at 8-hour intervals, meaning a position pays or receives the funding rate 21 times per week. Hyperliquid and dYdX settle every hour, resulting in 168 payments per week — eight times the frequency at identical annualized rates. For a $20.3M position at 40x leverage, as held by address 0x128e on Hyperliquid with a $82,236 liquidation price, even a modest negative funding rate compounds aggressively against the short holder. The James Wynn trajectory — 194 liquidations largely on Hyperliquid by March 2026 — illustrates what this compounding looks like over a multi-month horizon when directional conviction persistently opposes the funding environment.