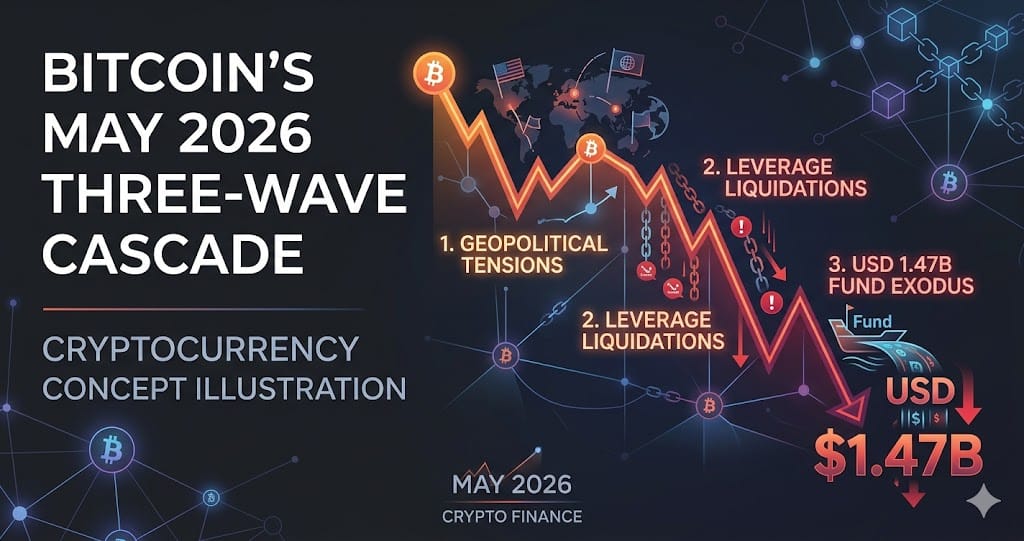

Bitcoin's May 2026 Three-Wave Cascade: Geopolitics, Leverage, and USD 1.47B Fund Exodus

Bitcoin suffered three cascade waves in May 2026 — a PPI shock, US-Iran collapse, and military strikes — wiping USD 1.47B from crypto funds in one

Bitcoin's May 2026 drawdown was not a single event but a three-wave cascade spanning 26 days, triggered by a PPI shock on May 13, a US-Iran diplomatic breakdown on May 22-23, and confirmed US military strikes near Bandar Abbas on May 26 — the last of which broke BTC below USD 80,000 and generated USD 300M in 24-hour liquidations.

The cascade was structurally pre-loaded before the first shock arrived. BTC perpetual funding rates had been negative for 46 consecutive trading days starting around March 1 — the longest such streak since the FTX collapse in November 2022 — while open interest recorded its fastest single-month growth of 2026. When the Fear and Greed Index crossed into Daily Greed on May 12, the market was one macro shock away from a chain reaction.

The Nine-Step Cascade Timeline in Full

The sequence began May 6 when the Fear and Greed Index ended a 108-day negative sentiment streak by reaching neutral, then crossed into Daily Greed on May 12. Within 24 hours, May 13 PPI data shocked markets and BTC fell to USD 78,704, initiating a multi-day liquidation phase through May 18 when single-session liquidations exceeded USD 500M. May 19 produced a flash crash to USD 76,270 with USD 657M cleared in one day.

A V-rebound on May 21 lifted BTC back above USD 80,000, but the move was structurally a short squeeze — the 46-day crowded-short buildup unwinding briefly — rather than genuine buying pressure. That false bottom was confirmed when the second wave hit May 22-23, with BTC printing USD 74,255, USD 941M in liquidations, and a single largest order of USD 32.4M. A brief broadest recovery on May 25 showed BTC +1.6%, ETH +1.5%, SOL +1.3%, BNB +2.4%, and DOGE +1.0% with liquidations falling to their lowest level since before May 12.

The May 25 recovery lasted under 24 hours. On May 26, CENTCOM confirmed self-defense strikes on Iranian missile launch sites and an Iranian vessel near Bandar Abbas, approximately 70 kilometers from the Strait of Hormuz. BTC broke below USD 80,000 again, Brent crude briefly crossed USD 100, and USD 300M in leveraged positions were liquidated within 24 hours, confirming the third and most geopolitically driven wave of the cascade.

Funding Rate Dynamics: Crowded Short, Short Squeeze, Long Trap

BTC perpetual contracts carried a negative 30-day average funding rate from approximately March 1 through April 15, spanning 46 consecutive trading days. This crowded-short structure meant most leveraged exposure before the cascade sat on the short side. On May 4, BTC reached USD 78,932 and Binance funding flipped from a 30-day average near -5% to +0.0043% in a single day. Long/short ratio data from that date showed 36.7% long versus 63.3% short — confirming the short concentration that would fuel the May 21 squeeze.

Altcoins displayed a distinct funding-positioning divergence during the cascade's middle phase. ETH funding sat at -0.0038%, SOL at -0.0036%, and XRP at -0.0025% — all negative — yet CoinGlass account-level data showed SOL at 73% long, XRP at 69.5% long, and ETH at 61.6% long. Retail accounts were net long while larger participants were net short on perpetuals, systematically harvesting the funding differential from the long side.

Exchange settlement mechanics amplified volatility unevenly. Binance, Bybit, and OKX use 8-hour funding settlement at 00:00, 08:00, and 16:00 UTC, allowing single-session spikes to accumulate before clearing. Hyperliquid, Kraken, and dYdX use 1-hour settlement, which smooths costs but provides more continuous feedback. During a multi-day cascade, the 8-hour cycle compounds negative carry on losing positions faster, creating larger per-session funding shocks for traders on the wrong side.

Machi Big Brother: Anatomy of a 31x Martingale Position

The on-chain trader known as Machi Big Brother held a combined USD 86M position consisting of USD 44.2M in BTC at 40x leverage (570 BTC) and USD 41.8M in ETH at 25x leverage (18,050 ETH), backed by only USD 2.78M in cross margin — a composite leverage ratio of approximately 31x. His ETH liquidation price was USD 2,206.50, within USD 100 of the mark price during the cascade, and his BTC liquidation price was USD 74,111 — nearly matching the May 22 cascade low of USD 74,255.

After being liquidated, Machi immediately opened a new position of 1,825 ETH at 25x leverage worth USD 3.87M. This behavior — rebuilding leveraged exposure immediately after a wipeout — is the operational signature of a Martingale strategy, where position size is maintained or increased after losses under the assumption prices will eventually revert. In a three-wave cascade spanning 26 days, that assumption fails because each wave resets the entry basis before mean reversion can complete, leaving each re-entry as exposed as the one before it.

Institutional Outflows and Open Interest: The Capital Structure Behind the Cascade

Crypto fund total outflows for the week ending May 26 reached USD 1.47B, with BTC funds recording their single largest weekly exit of 2026. This followed at least two consecutive weeks of BTC ETF net outflows totaling over USD 2B. The timing of peak outflows coinciding with the May 26 military escalation near the Strait of Hormuz is consistent with institutional risk-off behavior when geopolitical events cross from diplomatic to kinetic.

BTC perpetual futures recorded their fastest single-month OI growth of 2026 during the price run toward USD 80,000 in May. Expanding OI into a price surge, while funding rates remained historically negative, created what traders refer to as a hair-trigger market — a structure where leverage is concentrated and liquidation prices cluster, so even a moderate catalyst amplifies into outsized clearing events. The USD 941M liquidated on May 22-23 alone illustrates how quickly that energy can release.

HYPE, which ranked among the three hardest-hit altcoins in the May 15-19 first cascade phase, reversed sharply in the cascade's final stage, gaining approximately 60% in 48 hours driven by heavy short liquidations combined with a US spot ETF launch. By late May HYPE ranked 13th by market cap at USD 10.13B with a year-to-date gain of +40%. The same asset that absorbed heavy losses in wave one became a beneficiary in wave three, illustrating how cascade dynamics produce dramatically different outcomes for the same token depending on which phase is measured.

What to Watch

- BTC perpetual funding rate on Binance and Bybit: a return to multi-week negative territory signals renewed crowded-short buildup and potential for another short squeeze followed by a long trap sequence similar to May 2026

- BTC weekly ETF and crypto fund flow data: sustained outflows above USD 500M per week indicate institutional risk-off that has historically preceded or extended price cascades, as seen when the single-week USD 1.47B exit coincided with the third cascade wave

- Strait of Hormuz shipping status and US-Iran ceasefire developments: Bandar Abbas sits 70km from the strait, and any disruption to oil flows there correlates with crypto risk-off as broader markets reprice geopolitical risk premiums

- BTC perpetual open interest monthly growth rate: when OI growth accelerates to multi-month highs while price approaches resistance, it signals leveraged concentration that amplifies macro shocks — the exact pre-condition present before May 13

Ready to start trading?

Trade on Bitget Try CoinTech2uAffiliate links — we may earn a commission at no extra cost to you.

Related Articles

- Bitcoin's USD 941M Liquidation Cascade: What the May 2026 Crash Reveals

- 2026 Crypto Narratives: Equity Perps, AI Agents, and BTCFi Surge

- Bitcoin's May 2026 Cascade: How a PPI Shock Wiped USD 1.22 Billion in Two Days

Frequently Asked Questions

Why did Bitcoin fall three separate times in May 2026 instead of recovering after the first drop?

Each recovery was a false bottom rather than a structural reversal. The May 21 rebound was driven by a short squeeze after 46 days of crowded-short positioning, not genuine buyer demand. Once squeezed shorts rebuilt and longs accumulated above USD 80,000, the May 22-23 second wave cleared those longs down to USD 74,255. The May 25 recovery was interrupted within 24 hours by US military strikes near Bandar Abbas on May 26, which reset geopolitical risk premium across commodities and crypto simultaneously.

What made May 2026's funding rate environment unusually dangerous for leveraged traders?

BTC perpetual funding rates stayed negative for 46 consecutive trading days starting around March 1, the longest such run since the FTX collapse in November 2022. Persistently negative funding means the majority of leveraged traders were short, paying long holders a daily carry. When BTC broke upward to USD 78,932 on May 4 and funding flipped sharply positive in one session, it signaled the crowded short was unwinding — but it also meant longs were entering at the worst possible moment, just before the May 13 PPI shock triggered the first cascade wave.

How does Martingale leverage fail specifically during a multi-wave cascade?

A Martingale strategy maintains or increases position size after a loss under a mean-reversion assumption. Machi Big Brother's structure — USD 86M at 31x composite leverage backed by only USD 2.78M in cross margin — left essentially no buffer against a USD 100 adverse move in ETH. When liquidated on one wave, immediately reopening at 25x leverage (1,825 ETH, USD 3.87M) recreates the same exposure structure. In a cascade with three distinct waves over 26 days, there is insufficient time between waves for mean reversion to complete, so each re-entry faces the same liquidation risk without the margin base to survive another downdraft.